Medicare terms and a brief history

Medicare FAQ

We encourage clients to review their insurance plan every year

If You’re not Reviewing Your Medicare Coverage Every Year, You’re Probably Paying Too Much!

We Help You Customize Your Medicare Insurance

At some point, you and every other American close to or on Medicare will want the same thing—help! Help knowing when and how to sign up for Medicare. Help avoiding lifelong Medicare enrollment penalties. Help understanding Medicare insurance coverage options. Help deciding which Medicare insurance plan is “best.” Help shopping for and buying Medicare insurance policies. Help finding a Medicare insurance agent (that’s us!). Help reviewing Medicare insurance coverage annually.

If you buy the “wrong” type of Medicare insurance and then decide it’s not the best path for you, you may not be able to buy the “right” choice later on. Just because you made a choice at age sixty-five, doesn’t mean it’s still the right plan when you turn seventy.

Once you do make a choice, you’re generally locked into that choice for an entire year.

Making the wrong Medicare insurance choice can cost you thousands of dollars, even tens of thousands of dollars.

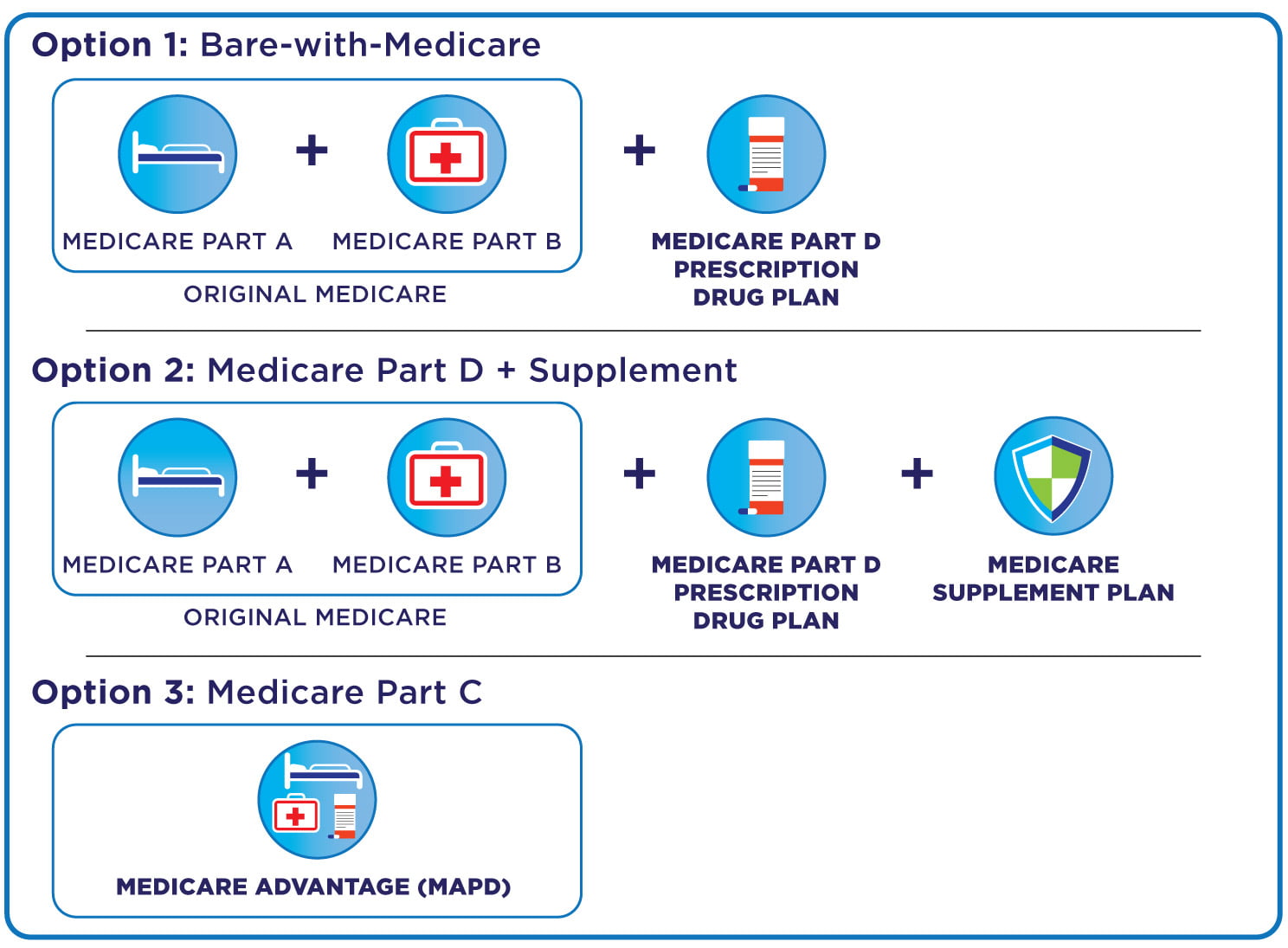

When you buy Medicare insurance, you have hundreds and perhaps thousands of Medicare insurance coverage choices to choose from. Choosing which of the three paths is right for you can be confusing. Once you choose a path, it gets even more complicated because the number and combination of Medicare insurance policies you can buy in either option can be absolutely dizzying.

That’s where Chicagoland Medicare comes in! Call or click to create an appointment today!

There Are Gaps in Original Medicare Parts A and B. The Right Medicare Insurance Plans Can Solve:

- Private hospital room or private nursing in the hospital

- Healthy food dollar amount allowances at grocery stores

- Adult daycare visits and personal home helpers

- Lifestyle drugs, including erectile dysfunction prescriptions

- Air conditioner allowances for people with COPD and asthma

- Transportation to doctor’s appointments

- Nutritional programs, personal trainers, and access to spas

- Grocery delivery

- Flexible dollar amount allowances for healthcare-related items at select retailers (sometimes in the hundreds of dollars per year)

- Acupuncture and massage therapy

- Gym memberships or fitness classes

- Weight management programs

- Dental insurance and dentures

- Routine eye exams and glasses

- Routine hearing tests and hearing aids

- In-home safety assessments and services

There are generally three Medicare plan coverage paths to choose from.

Medicare Terms

Select each Question to reveal additional information:

What is Medicare?

Original Medicare is medical insurance for people over the age of sixty-five, and people under sixty-five with a long-term disability, or those who have certain disabilities like End-Stage Renal Disease (ESRD) or Amyotrophic Lateral Sclerosis (ALS), commonly known as Lou Gehrig’s disease. Once you’re eligible, there’s no need to medically “qualify” for Medicare—you get it regardless of your current health. Read More »

What is Medicare Part A?

This is hospital coverage, hospice, and skilled nursing care. For most people, this doesn’t cost you anything; it’s an entitlement program because you and your company have essentially already paid your portion through payroll taxes while you or your spouse were working. Read More »

What is Medicare Part B?

This covers doctors’ visits, services provided by doctors while in the hospital, ambulance rides, outpatient procedures, durable medical equipment (things like oxygen machines, CPAP devices, blood sugar monitors, diabetic test strips, etc.), and a very small number of prescription drugs (which are often extremely expensive). Read More »

How Do You Select the Medicare Insurance Companies You Choose to Do Business With?

We only partner with ‘A’ rated, household name, established Medicare insurance companies who offer Medicare Advantage, Medicare Supplement, Medigap and Medicare Part D plans in Illinois, Indiana and Wisconsin. Read More »

What is the Medicare Part B Late Enrollment Penalty?

If you’re eligible to get Medicare Part B, and you actively choose not to enroll in it for some reason, not only will you not have coverage for some healthcare items, but if you ever do want to sign up for Part B, you’ll get penalized for the rest of your life. Read More »

What is Medicare Part C?

This is also called Medicare Advantage. Medicare Advantage plans are only sold by authorized insurance companies. You cannot buy a “federal” or a “public option” Medicare Advantage plan. Medicare Advantage comes in a few shapes and sizes, but the vast majority of them are technically called “Medicare Advantage-Prescription Drug” plans. Read More »

What is Medicare Part D?

Medicare Part D helps pays for retail prescriptions, usually at your local pharmacy or via mail-order. Part D does not cover medical procedures—it only covers prescription drugs. These are only sold by insurance companies. Read More »

What is the Medicare Part D Late Enrollment Penalty?

There’s also a Medicare Part D late enrollment penalty. According to Medicare, the late enrollment penalty is an amount that’s permanently added to your Medicare drug coverage (Medicare Part D) premium. Read More »

What is Medicare Advantage?

Medicare Advantage plans with Prescription Drug (MAPD) cover your medical costs as well as your Medicare Part D prescription drug coverage. Remember, these are Medicare Part C plans. These are combo plans—they cover the medical benefits of Original Medicare Parts A and B, as well as D. Approximately 45% of the sixty-seven million people on Medicare use this option. Read More »

What are Medicare Advantage Provider Networks?

There are three types of Medicare Advantage plan networks – PPO, HMO, & HMO-POS. There are some minor exceptions but not enough to note here. Read More »

What is Medigap or Medicare Supplements?

Medicare Supplement plans, also referred to as “Medigap” plans, Medicare Supplements are insurance policies that help cover the deductibles, coinsurance and copays Original Medicare A and B doesn’t pay for. These are also only sold by insurance companies. In order to buy a Medicare Supplement plan, you must have Original Medicare Parts A and B. Read More »

Can I change my Medicare Supplement or Medigap policy during Open Enrollment?

Want to drop your Medicare Part D Prescription Drug + Medicare Supplement plan and go to an all-in-one Medicare Advantage plan during the AEP between October 15 and December 7 of each year? No problem! Want to switch back later? Potentially a big problem! Read More »

What is the Medicare Supplement or Medigap Open Enrollment Period?

Depending upon the rules of your particular state, you may have to go through medical underwriting to purchase a Medicare Supplement plan outside of a special window when you turn sixty-five. Medicare Supplement plans are not like Original Medicare Parts A and B, Medicare Part D, or Medicare Part C (Medicare Advantage plans) in that Medicare Supplement insurance companies can deny you coverage based on your health. Read More »

What is the Medicare Annual Enrollment Period (AEP)?

Depending upon the rules of your particular state, you may have to go through medical underwriting to purchase a Medicare Supplement plan outside of a special window when you turn sixty-five. Medicare Supplement plans are not like Original Medicare Parts A and B, Medicare Part D, or Medicare Part C (Medicare Advantage plans) in that Medicare Supplement insurance companies can deny you coverage based on your health. Read More »

What is the Medicare Advantage Open Enrollment Period?

Although the Annual Election Period (AEP) ends on December 7 every year, that does not necessarily mean that you’re completely out of luck if you still want to make a change after December 7. With the AEP occurring around the holidays, it’s no wonder some folks simply miss it. Read More »

What can't you do during the Medicare Advantage Open Enrollment Period?

If you decide to drop your Medicare Advantage plan and buy a Medicare Part D Prescription Drug plan during the OEP, you’ll be bumped off of your Medicare Advantage plan and default back to Original Medicare A and B for your medical insurance coverage. Read More »

Top 5 Tips for Choosing the Best Medicare Insurance Plan for Your Needs

When selecting a Medicare plan, it’s important to consider your medical needs and budget. It also helps to review how each plan compares in terms of prescription drug coverage and provider network options. Read More »

Understanding Medicare Eligibility in Illinois, Indiana, and Wisconsin

Whether you are still working or have retired, becoming eligible for Medicare is a significant milestone. Now is the time to review your benefits and take appropriate action. Read More »

How We Can Help

Book

Free Consultation

Medicare part D

The tiers and Phases of Medicare Part D

benefit phases of Medicare Part D Prescription Drug Plan:

Medicare sets a “standard” or “minimum” Medicare Part D Prescription Drug Plan design for insurance companies to offer. Many offer plans that cover the gaps outlined below, usually for a higher premium.

There are four benefit phases of every “standard” Medicare Part D Prescription Drug Plan, and they reset every year on January 1. This isn’t something you can pick or change; it’s what the federal government decided was the way these would work. However, Medicare insurance companies can offer better benefits than just the standard plans, and many do. For example, there are many plans for sale that eliminate the deductible in Phase 1 but still follow this four-phase approach.

A byproduct of this four-phase approach is that, very likely, you won’t pay the same amount for the same prescription at the pharmacy for the entire year. It’ll be a moving target as you wander through these stages, so don’t be surprised. There’s nothing for you to track; the Medicare insurance company tracks all of this for you. You may be able to use mail-order to get lower prices, and of course, check other in-network pharmacies.

PHASE 1—This is the deductible phase. In 2023, you pay 100% of your prescription costs until you are at $505 out-of-pocket. This amount goes up every year, sometimes a little, sometimes a lot. Again, there is good news—there are a number of Medicare insurance companies that offer plans with zero deductible.

PHASE 2—This is called the Initial Coverage period. In 2023, after Phase 1, you pay a copay for each prescription until the total drug costs (what you and the Medicare insurance company spend, including any deductible) reach $4,660. This also typically goes up every year.

PHASE 3—This is called the Coverage Gap or “doughnut hole” and kicks in when the total prescription spending is between $4,660 – $7,400 (2023). This stage has really improved for consumers over the last few years. The insurance company doesn’t pay any benefits at this stage, but you get discounts from drug manufacturers and the government during this stage. You exit the coverage gap when your total out-of-pocket cost on covered drugs (not including premiums) reaches $7,400 for the year. Your out-of-pocket cost is calculated by adding together all of the following: yearly deductible, coinsurance, and copayments from the entire plan year, and what you paid for drugs in the coverage gap (including the discounted amounts you didn’t pay in that stage). There’s nothing for you to do or track here.

PHASE 4—This is called the Catastrophic Coverage phase. Once your out-of-pocket cost totals $10,516.25 (2023) in a given year, you exit the gap and get catastrophic coverage. In the catastrophic stage, you will pay a low coinsurance or copayment amount (which is set by Medicare) for all of your covered prescription drugs. That means the plan and the government pay for the rest—about 95% of the cost. You will remain in this phase until January 1 of the next year.

Medicare Part D Tiers:

Within the formulary, prescription drugs will be categorized into tiers. These tiers are usually labeled 1-5, each with different copays or coinsurance amounts. Tier 1 drugs are usually the cheapest, Tier 5 the most expensive.

Tier 1: Preferred Generics

Tier 2: Non-preferred Generics

Tier 3: Preferred Brand Drugs

Tier 4: Non-preferred Brand Drugs

Tier 5: Specialty Drugs

Formulary tiers vary from plan to plan; sometimes, they come with six tiers. Soon, Medicare is expected to allow seven tiers.

Medicare Part D Prior Authorization

Medicare insurance companies may require your doctors or other health providers to prove you need certain drugs before you can fill a prescription at the pharmacy. To do this, the insurance company could ask them to submit their medical reasoning, medical history, lab results, current symptoms, and treatment history. Most, if not all, Medicare Part D benefits have a Prior Authorization component, but the drug categories and individual drugs within the programs vary by company and the plan they’re on. There are two types of reviews: Standard and Expedited. If you’re having trouble getting approvals or need the review to happen quickly, you may want to specifically ask for an Expedited Review.

Prior Authorizations are typically found on brand-name prescription drugs that have a generic option available, drugs that have the potential to be abused, drugs used for cosmetic reasons, drugs that may have adverse health effects, or that are dangerous when combined with other medications.

Medicare Part D Networks

Most Medicare Part D plans will come with a preferred network and a non-preferred network, although what they call them might be different. Get your prescriptions from preferred pharmacies and your costs will be lower. Get them from non-preferred pharmacies and they’ll be higher. Essentially, insurance companies contract better pricing (for them and often, for you) with those preferred brick-and-mortar or mail-order pharmacies and do not get the same deals with non-preferred pharmacies.

Sound confusing? It kind of is–until you get used to it. There are a few things to remember:

- Each Medicare insurance company selling Medicare Part D Prescription Drug Plans must offer at least the minimum plan design described above. A large number of them also sell enhanced plans that eliminate the deductible and provide additional coverage through stages 2-4.

- Each Medicare insurance company tracks the four phases as you go through them for you. There’s nothing for you to do or track.

- Benefits reboot every January 1 for all Medicare Part D Prescription Drug Plans. (They also reboot January 1 for Prescription Drug Plans embedded into a Medicare Advantage plan, too.)

- There is no 4th quarter “carry-over” feature like some employer-based health insurance plans have. So, if you were used to getting “credit” in the following year for paying deductibles or co-insurance in the 4th quarter in the prior year, Medicare doesn’t do that. Hypothetically, you could pay your deductible on December 31 and then pay it again on January

- Each insurance company has its own formulary, which is a list of drugs they cover on their plan. No two companies have the exact same one, but Medicare makes them cover at least two drugs in each “class” of medications that treat a condition. They might not be the drugs you take, but some companies might cover yours. Yes, they change the drugs covered in the formularies and also change how much they cost every year. That’s why it’s important to make certain you check every October to see if you’re still in the best plan for you.

- Each insurance company has its network of preferred, or “in-network,” pharmacies you can go to. Many have “preferred” and “non-preferred” lists, and you’ll get the best bang for your buck at the “preferred” pharmacies. Why? Essentially, insurance companies contract better pricing (for them and often, for you) with those preferred pharmacies and do not get the same deals with non-preferred pharmacies.

- Many insurance companies offer mail-order prescription delivery, and it’s often cheaper than filling them at your local pharmacy.